Bitcoin is once again being pulled between macro headlines, institutional flows, and structural shifts inside the mining industry. On the surface, price action looks constructive but underneath, the dynamics are becoming more complex. Capital is flowing in through ETFs and corporate treasuries, while miners are selling at record pace and reallocating toward new strategies. This edition breaks down what’s really driving the market and what it means for the second half of this halving cycle.

Macro Volatility Returns to the Driver’s Seat

ETF Flows Rebound

Strategy Doubles Down at Breakeven

Forced Distribution Public Miners

When Hashprice Breaks the Mining Model

The Sell-Off Had a Second Motive

Hashrate Pullback Makes the Strategic Shift Visible

Hardware Prices Collapsed

Halving Cycle at the Midpoint

I’m excited to be moderating a panel at The Bitcoin Conference 2026 in Las Vegas, one that goes straight to the core of mining profitability. The session, “Squeezing Profit from the Margins: Uncovering Stranded Sats in Mining Operations,” will take place on Wednesday at the Energy Stage.

Hope to see you there. If you’d like to meet in person, just reply to this email or book a meeting through the conference app.

Macro Volatility Returns to the Driver’s Seat

Bitcoin briefly dropped below $75,000 before rebounding sharply, following comments by Donald Trump suggesting that a ceasefire between Iran and the U.S. is “highly unlikely” to be extended without a deal before the April 22 deadline. The move highlights how quickly macro headlines can impact price action.

From a technical perspective, Bitcoin has regained momentum. It has moved back above its 100-day moving average, after already reclaiming the 50-day SMA earlier this month.

The next key level to watch is the 200-day SMA, currently around $86,000. This level previously acted as support in Q4 2025 and will likely be a critical resistance zone. A break above it would strengthen the case for a continued bullish trend.

However, the recent price action reinforces a familiar pattern in the current market environment: Bitcoin is highly reactive to macro catalysts. This means the next move won’t be dictated by technicals alone, geopolitics and broader market sentiment remain key drivers.

Source: TradingView

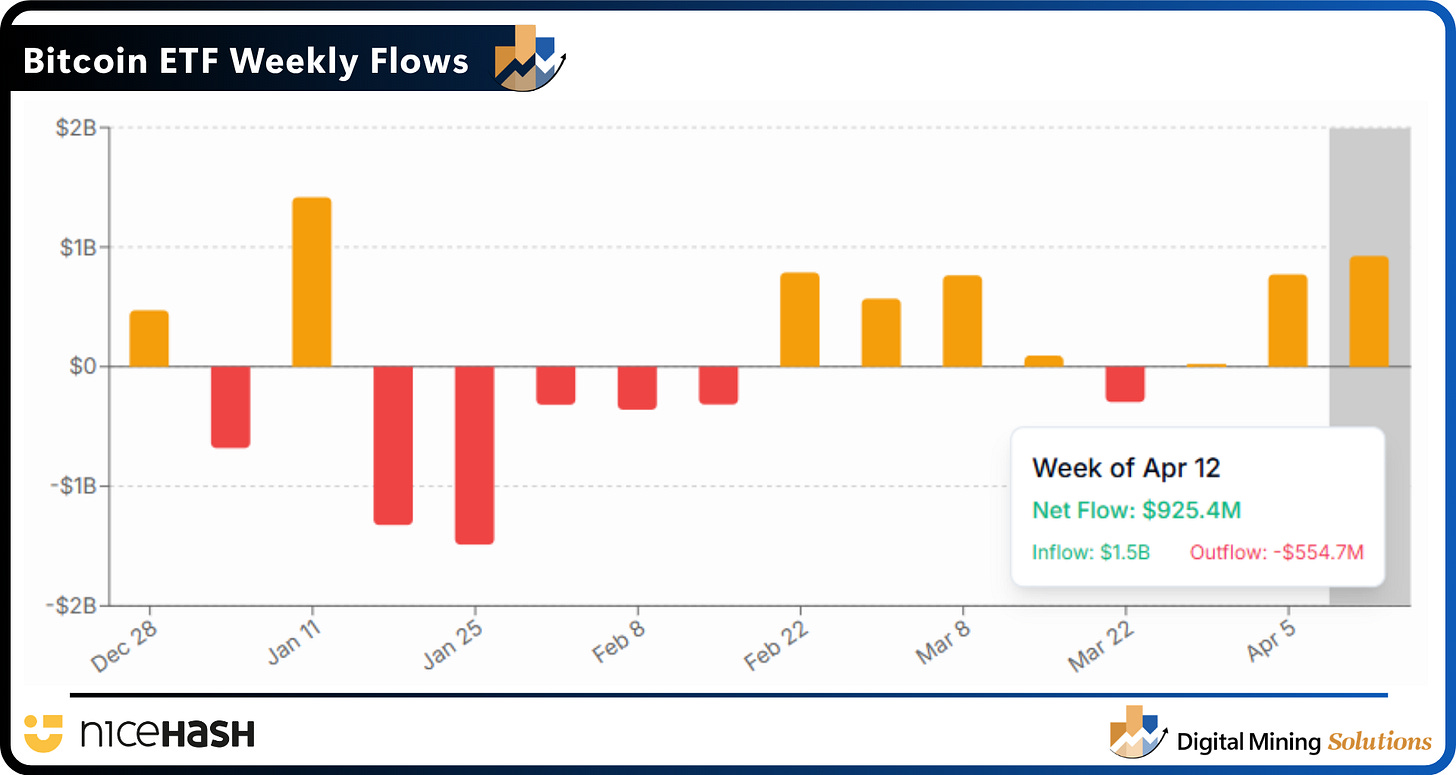

ETF Flows Rebound

Spot Bitcoin ETFs saw a strong rebound last week, with nearly $1 billion in net inflow. The highest weekly total since mid-January. Year-to-date flows have now turned positive for the first time since January, signaling a shift in momentum after a weaker start to the year.

Source: Coinflows

Total net assets across U.S. spot Bitcoin ETFs have climbed back above $100 billion, still below the peak of around $165 billion in October last year but showing first signs of recovery. The key question now: does this renewed flow momentum translate into durable price support?

Strategy Doubles Down at Breakeven

MicroStrategy has executed its largest Bitcoin purchase in over a year, adding 34,164 BTC for $2.54 billion at an average price of $74,395. The accumulation took place between April 13 and 19 and pushes Strategy’s total holdings to 815,061 BTC, with a cumulative investment of $61.56 billion. This move comes on the back of already aggressive buying earlier this month, including a $1 billion purchase just last week.

What stands out is the timing. Bitcoin has been trading close to Strategy’s average cost basis of roughly $75,500, placing the firm near breakeven. But rather than slowing down, Strategy is leaning in.

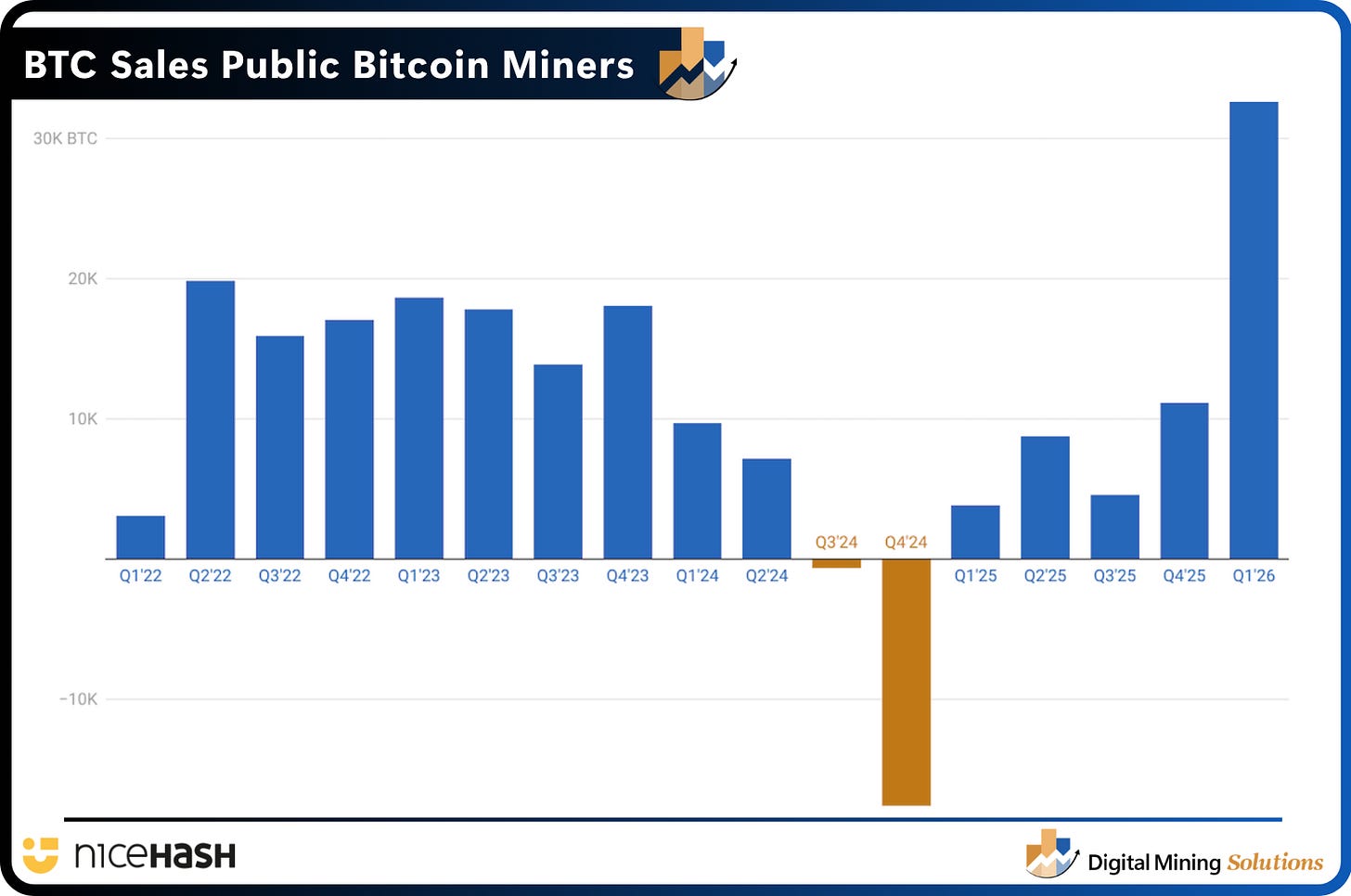

Forced Distribution Public Miners

While ETFs and corporate buyers like MicroStrategy are absorbing supply, another key cohort is moving in the opposite direction. Public miners becoming net sellers again. Public Bitcoin miners have liquidated their BTC reserves at a pace not seen since the depths of the last bear market, as a prolonged squeeze in mining economics pushes operators into survival mode.

Several major players, including MARA Holdings, CleanSpark, Riot Platforms, Cango, Core Scientific, and Bitdeer, have already sold more than 32,000 BTC in Q1 2026, based on data analyzed by TheEnergyMag. The dataset is still incomplete, with several first-quarter earnings reports yet to be published.

Even so, the scale is already significant. Q1 sales have surpassed total net liquidations for all of 2025 and set a new industry record, exceeding the roughly 20,000 BTC sold in Q2 2022 during the market turmoil following the Terra-Luna collapse.

The reversal is striking. Just over a year ago, miners were in accumulation mode—adding 17,593 BTC in 2024 and pushing combined reserves above 100,000 BTC.

Source: TheEnergyMag

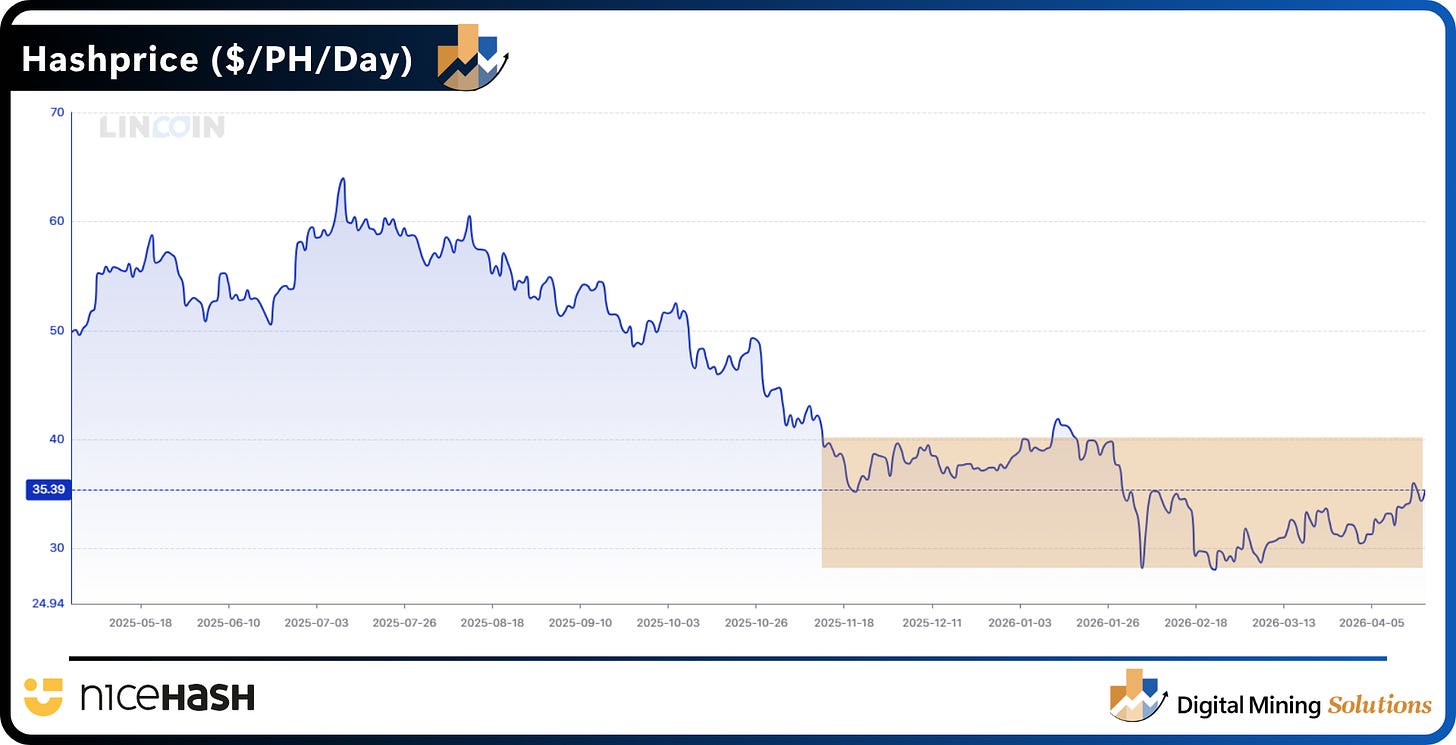

When Hashprice Breaks the Mining Model

The shift by public miners is mainly being driven by sustained weakness in mining margins. Hashprice is has been below $40/PH/s for the majority of 2026. At these levels, margins are heavily compressed and some public miners even outright negative.

Source: Lincoin Lens

The Sell-Off Had a Second Motive

Low hashprice wasn’t the only reason public miners liquidated record volumes of BTC in Q1. For several operators, the sell-off was a deliberate funding mechanism for the pivot to AI/HPC infrastructure, a strategic choice, not just a survival reflex.

Three examples stand out. Core Scientific sold roughly 1,900 BTC in January alone and committed to liquidating substantially all remaining holdings through Q1, directing proceeds toward its high-density AI colocation buildout, anchored by a $10.2 billion, 12-year deal with CoreWeave. Cango sold 4,451 BTC for ~$305 million in February, using the full amount to repay a Bitcoin-collateralized loan and free balance sheet capacity for its AI infrastructure push. Bitdeer went furthest, reducing its treasury to zero to fund data center expansion, while simultaneously ramping its proprietary SEALMINER hashrate to 70 EH/s. Taken together, it can be concluded that it was not just a distressed sale, but in various cases a capex decision.

Source: BitcoinMiningStock.io

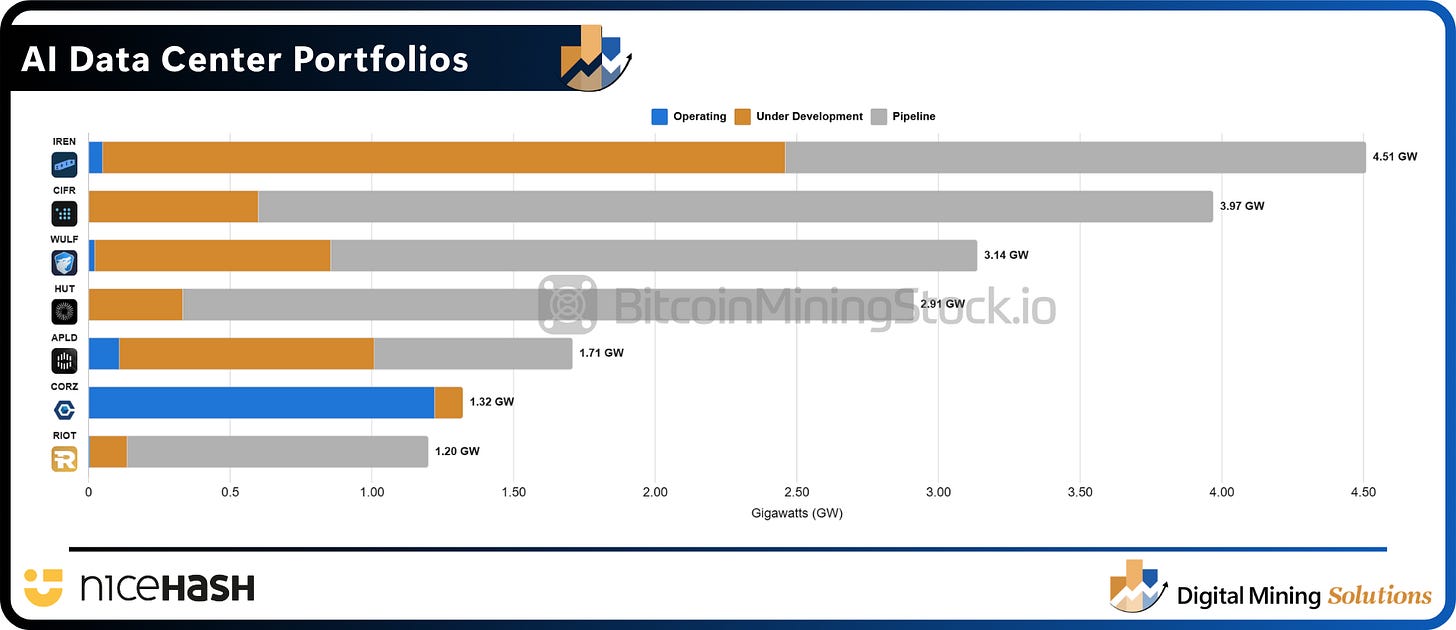

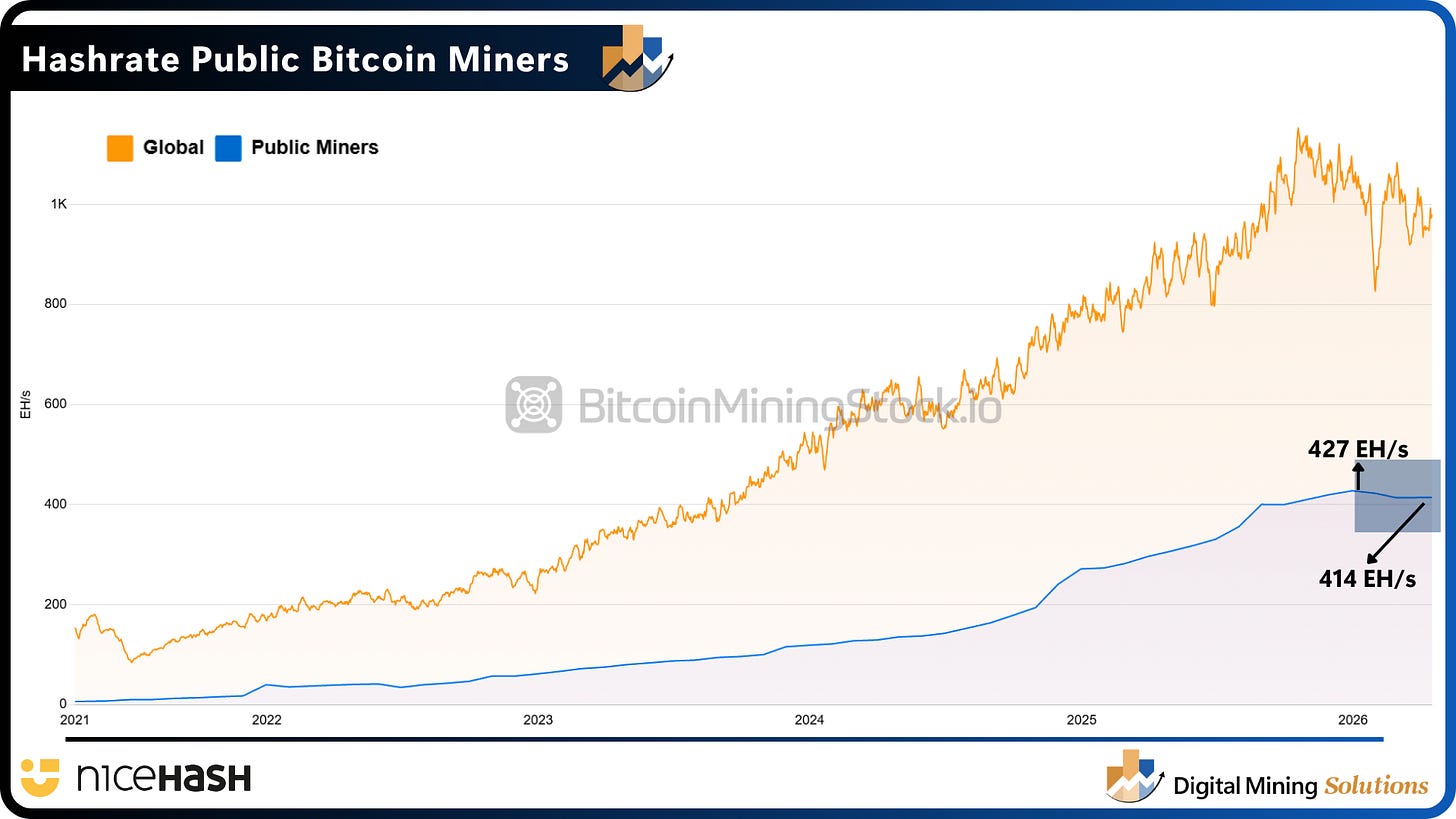

Hashrate Pullback Makes the Strategic Shift Visible

The growing focus on AI/HPC is starting to become visible in public miner hashrate. Aggregate hashrate has now declined for three consecutive months, falling from 427.8 EH/s to 412.7 EH/s.

Source: BitcoinMiningStock.io

This trend isn’t uniform across the board. The top three players Bitdeer, MARA Holdings, and CleanSpark have still expanded their fleets by 2.2% to 9.5% over the past 30 days.

The decline is largely driven by a smaller group of operators scaling back aggressively. Cango stands out, taking 27% of its fleet offline over the past six months, including 19% in the last month alone. Looking over a longer timeframe, several miners have posted double-digit hashrate declines, with Core Scientific (-10.8%) and Cipher Mining (-49.6%) among the most notable.

Hardware Prices Collapsed

Softened demand is driving ASIC prices to levels not seen since the last bear market trough. For well-capitalised buyers with low power costs, the entry point is historically attractive. The hardware is cheap but the time to get a return on the investment this halving epoch is running out.

Source: HashrateIndex

Halving Cycle at the Midpoint

The 2024 halving occurred at block 840,000 on April 20, 2024, cutting block rewards from 6.25 BTC to 3.125 BTC. The next halving is expected at block 1,050,000 in 2028. On April 13, 2026, the network passed block 945,000, marking the midpoint of the current halving cycle.

Source: Mempool.space

This milestone offers a natural moment to step back. In the first half of this epoch, how have different mining revenue strategies held up? And as we move into the second half, given current levels of hashprice, what will miners need to adapt in order to stay competitive?

If you found this useful, forward it to someone running a mining operation or who is investing in Bitcoin mining.